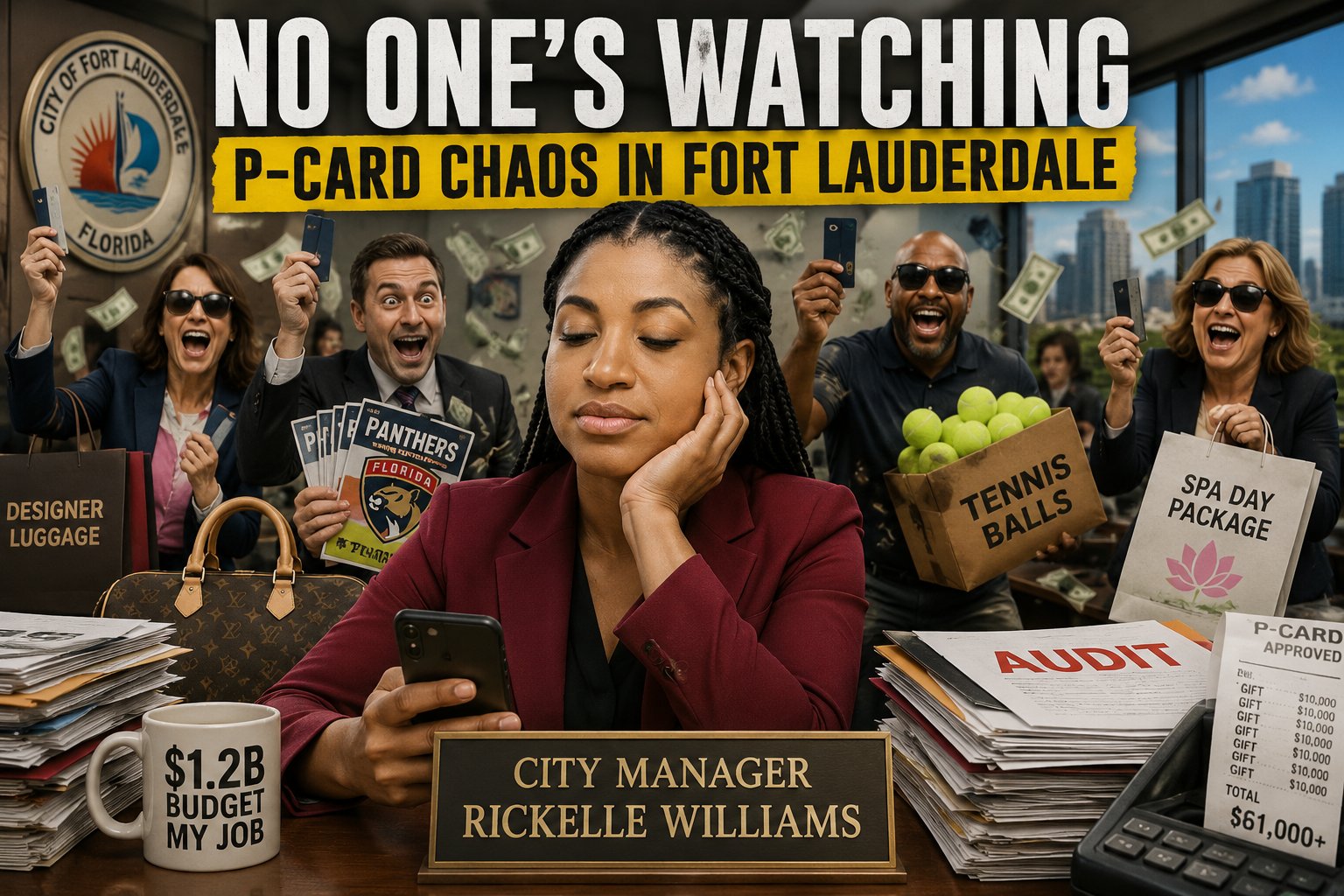

Fort Lauderdale Audit Exposes Questionable Spending, Missing Controls, and Vendors Linked to a Massage Parlor Address

City Credit Card Program Under Fire After Auditors Uncover Luxury Purchases, Unreported Fraud, and Major Oversight Failures

FORT LAUDERDALE, Fla. — A new City Auditor report has revealed widespread failures within Fort Lauderdale’s purchasing card program, exposing questionable spending, weak oversight, missing documentation, and procurement practices that have left city commissioners demanding answers about how taxpayer dollars are being managed.

Presented during the May 6, 2026 City Commission meeting, the audit paints a troubling picture of a program that appears to have drifted far from its original purpose. Purchasing cards, commonly known as P-cards, are intended to provide city employees with a streamlined way to make small dollar operational purchases and emergency expenditures without navigating lengthy procurement procedures. Instead, auditors found examples of luxury purchases, unexplained gifts, inactive controls, missing agreements, delayed card cancellations, and tens of thousands of dollars in fraudulent charges that went unnoticed.

Perhaps most alarming, auditors discovered that more than $61,000 in hardware supply purchases were routed through unusual third party vendors rather than established suppliers, leading investigators to a business address linked to a local massage parlor.

The Massage Parlor Connection

The audit’s most eyebrow raising finding involved a series of hardware related purchases totaling approximately $61,000. According to auditors, the issue was not that city employees were purchasing massages with taxpayer funds. Rather, investigators discovered that hardware purchases had been routed through intermediary vendors whose backgrounds raised serious concerns.

When auditors examined one of the companies receiving public funds, they found the business was registered to a mailing address associated with a local massage parlor. The finding immediately raised questions about vendor verification procedures and whether proper procurement safeguards were being followed before taxpayer dollars were sent to outside entities.

The discovery suggests that city purchasing controls may have been so weak that payments were being directed to businesses with little apparent connection to the products being purchased.

Luxury Spending Raises Questions

The audit also identified a series of purchases that appear inconsistent with the intended purpose of the purchasing card program.

Among the expenditures flagged by auditors:

More than $10,000 spent on Florida Panthers tickets without a clearly documented public purpose.

Roughly $10,000 worth of tennis balls reportedly categorized as gifts, with auditors questioning who received them and why city funds were used.

Approximately $1,800 in leather luggage purchased without sufficient justification.

While some expenditures may ultimately have legitimate explanations, auditors found documentation supporting those purchases was often incomplete or missing entirely. The findings have prompted renewed concerns about whether city employees and supervisors have been adequately following procurement policies.

Fraud Went Unnoticed

One of the most significant findings involved nearly $20,000 in fraudulent charges discovered on city purchasing cards. According to the audit, the charges remained active and unreported for months. Auditors concluded that monthly reconciliation procedures either were not being performed properly or were being approved without meaningful review.

In a properly functioning purchasing card program, fraudulent transactions should be identified quickly through monthly statement reviews and verification processes. The fact that the charges went unnoticed has raised concerns that oversight mechanisms existed largely on paper but were not being actively enforced.

Employees Had Cards Without Required Agreements

The report also revealed numerous administrative failures throughout the program. Auditors found that some employees possessed active city purchasing cards despite never signing mandatory cardholder agreements. Those agreements are intended to ensure employees understand the legal requirements, ethical obligations, spending limitations, and personal accountability associated with using taxpayer funded credit cards. Without signed agreements, city officials may face greater difficulty enforcing accountability when improper purchases occur. The finding suggests basic internal controls were not consistently followed across departments.

Former Employees Kept Active Cards

Another major concern involved delays in deactivating purchasing cards after employees left city employment. According to the audit, coordination failures between Human Resources and department management allowed some former employees to retain access to active city credit lines after separation from employment. Such delays create obvious financial and security risks, particularly when public funds are involved. Government auditors routinely consider timely deactivation of purchasing privileges to be one of the most basic internal financial controls.

Supervisors Failed to Verify Purchases

The audit further concluded that supervisors frequently approved monthly purchasing card statements despite missing receipts, incomplete documentation, and unanswered questions regarding expenditures. Many transactions lacked detailed supporting records.

In some cases, auditors found no evidence that supervisors had performed meaningful reviews before signing off on expenditures. The result was a system where policy violations could occur repeatedly without triggering corrective action.

Pressure Mounts on City Hall

The findings have increased pressure on City Manager Rickelle Williams, who assumed leadership of the city’s administration in 2025 and oversees Fort Lauderdale’s approximately $1.2 billion municipal budget. Commissioners and residents are now calling for significant reforms to the purchasing card program.

Among the proposals being discussed are freezing non-essential purchasing cards, conducting forensic reviews of historical transactions, strengthening vendor verification requirements, increasing supervisory accountability, and implementing stricter auditing procedures.

The audit did not accuse city officials of criminal conduct. However, it did reveal a pattern of lax enforcement, weak controls, and insufficient oversight that allowed questionable spending and administrative failures to persist.

Bigger Questions About Accountability

Beyond the individual purchases, the report raises a broader question about accountability inside local government. The policies designed to protect taxpayer dollars already existed. Employees were supposed to sign agreements. Managers were supposed to verify purchases. Cards were supposed to be canceled promptly. Fraud was supposed to be identified through routine reviews.

Yet auditors found failures at nearly every level of the system. The result is an audit that has become less about tennis balls, Panthers tickets, or questionable vendor addresses and more about whether Fort Lauderdale’s financial safeguards were functioning at all.

For city leaders, the challenge now is restoring public confidence that taxpayer money is being spent appropriately and that the controls intended to protect public funds actually work. The coming months will determine whether this audit becomes merely another embarrassing government report or the catalyst for a major overhaul of how Fort Lauderdale manages public spending.

Linda Short the Finance Director failed to do her job.