American Express: From Prestige to Predatory

And the Internet Is Packed With Receipts…

“American Express built its brand on exclusivity, loyalty, and reliability. But today, many longtime cardholders are at the mercy of an algorithm that slashes their credit lines without warning leaving even million-dollar customers stranded.” – Patrick Zarrelli

From Heritage to Rampant Algorithmic Abuse of Customers

For most of its 174-year history, American Express stood for prestige. It was the card of business leaders, global travelers, and professionals who needed stability and premium service. Membership wasn’t just about access to credit; it was about trust, concierge assistance, and the confidence that Amex would back its cardholders in a crisis.

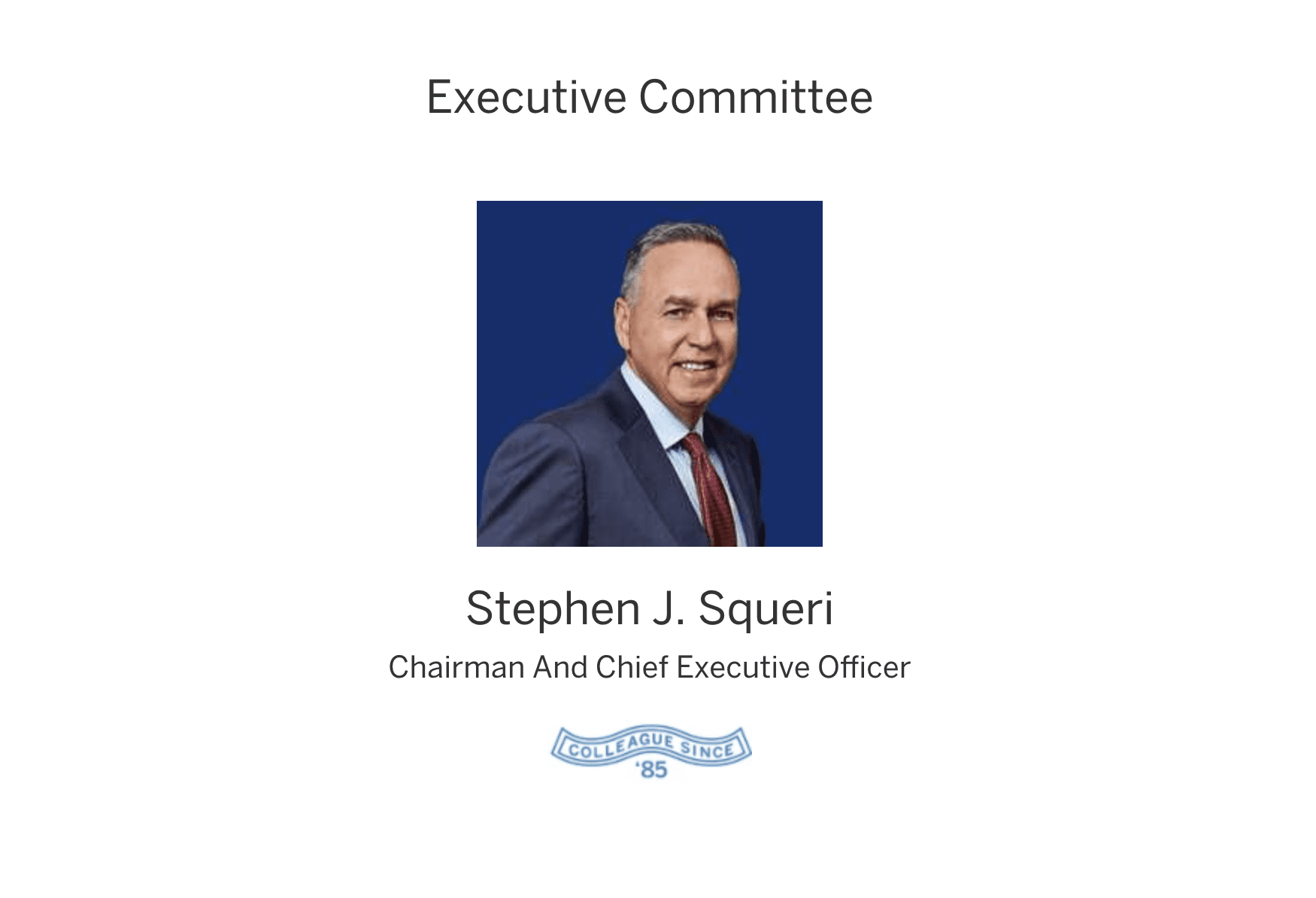

That legacy has been radically reshaped under the leadership of CEO Stephen J. Squeri, who has been at the helm since 2018. Squeri and the American Express Board of Directors have aggressively leaned into a computer-driven account review model. In practice, this means customer service agents now admit they have no authority to override automated credit decisions. The system is rigid, opaque, and merciless, designed to flag and punish perceived risks with instant credit line cuts.

What makes this shift so dangerous is the lack of transparency. Customers are not notified in advance when their accounts are flagged for review, nor are they given the opportunity to contest or resolve issues before their limits are slashed. The result is a wave of algorithmic punishment that ignores years of on-time payments and loyalty.

Instead of human judgment, Amex cardholders are now at the mercy of a black-box risk engine that prioritizes statistical models over lived customer history. This has led to what many are calling one of the most abusive and punitive credit systems ever built, a system that reduces real people to data points and strips away financial security without warning.

The Million-Dollar Customer Who Got Stranded

Over three years, this cardholder spent more than $1 million with Amex, well over $300,000 per year.

While traveling internationally, Amex cut his revolving credit line mid-journey, leaving the card unusable at the airport, despite having made a large cash transfer payment that day, the card now had a zero usable balance.

He asked Amex to free up $100 to finish the travel day and settle up upon returning to the U.S. and Amex refused.

Months later, a $500 autopay hiccup, corrected the next day, triggered another large credit line slash with no warning.

Most recently, after he made a $10,000 payment, Amex reduced his credit line by the same $10,000, instantly erasing that breathing room from his monthly budget and forcing another emergency cash shuffle.

This isn’t “premium service.” It’s a computerized tripwire built to leave you in a jam.

Not an Outlier: Widespread Reports Have Appeared on Reddit, BBB, and CFPB

The Better Business Bureau (BBB) a long-standing benchmark of corporate credibility refuses to accredit American Express. The company holds a zero rating, weighed down by hundreds of unresolved complaints. The pages read like a pattern: sudden credit line cuts, ruined credit scores, customers stranded at airports or denied in emergencies. For a company that built itself on white-glove loyalty, this is reputational freefall.

This collapse of trust isn’t just anecdotal it’s been backed up by federal enforcement. American Express has repeatedly faced scrutiny from the Department of Justice (DOJ) and the Consumer Financial Protection Bureau (CFPB) for deceptive and discriminatory practices.

In 2025, Amex paid $108.7 million to settle allegations it used “dummy accounts” and misleading marketing tactics in its small business operations.

The same year, it agreed to another $138 million settlement over a wire fraud investigation tied to false claims about tax treatment of its wire transfer products.

In earlier years, the DOJ forced Amex into a $55 million forfeiture for Bank Secrecy Act violations linked to anti–money laundering failures.

The CFPB has also taken action, finding Amex discriminated against consumers in Puerto Rico and U.S. territories by offering inferior credit terms compared to customers in the states, a case that led to nearly $100 million in remediation.

Together, these enforcement actions paint a picture of a company not only willing to mislead customers but one that has had to be dragged into compliance by regulators time and again. When you combine a zero rating at the BBB, pages of consumer complaints, and over $230 million in DOJ and CFPB settlements, the conclusion is unavoidable: American Express has abandoned its legacy of trust. It is now a company defined by opaque algorithms, abusive reviews, and a trail of federal penalties that underscore its collapse from prestige to predator Cases of drastic, no-notice credit-line cuts are everywhere on Reddit, the Better Business Bureau, and the CFPB complaint database all show the same pattern.

Reddit is flooded with near-identical stories: sudden, drastic reductions (e.g., $16,500 to $1,000 overnight), lines slashed “on all cards,” and reductions after on-time PIF histories, often without advance notice and with canned “risk” explanations.

BBB complaints show customers blindsided by limit drops that hurt credit scores and undercut planned spending, including cases where Amex reduced limits after customers made sizable payments.

In the CFPB public database, multiple narratives describe global limit cuts, sudden declines on essential purchases, and accounts shut or restricted with no clear justification.

The pattern is consistent: computer-driven risk models cutting available credit first and asking questions later.

Amex’s Defense vs. Customer Reality

Ask an Amex supervisor why there’s no 30-day warning, and you’ll hear a version of this:

“If we give notice, people will just run up their credit lines.”

That logic collapses under scrutiny. Amex has long marketed charge-card behavior, pay in full each month, and targets affluent spenders. The customers getting squeezed aren’t gaming the system; they’re funding it. Years of on-time, large payments are being discounted by an algorithm that treats any blip as a red flag.

From White-Glove to Watchlist

If anything unusual happens on your credit report, or if you miss even a minor payment by a day, Amex’s automated system can treat it like a crisis and obliterate your credit lines overnight. There is no grace period, no human review, no chance to explain. One small hiccup in the grand scheme of a spotless account history can trigger massive reductions that wreck your monthly budget, torpedo your credit score, and leave you scrambling to move money in an instant. What once was a safety net for professionals and travelers has become a liability waiting to explode, capable of upending your financial life without warning. American Express used to be the safety net especially for travelers and business owners who value stability. Now the experience looks like this:

No warning: You discover the cut at the register or gate.

No flexibility: Even $100 grace during an airport emergency is denied.

No memory: Your history of high-dollar, on-time payments means nothing to the model.

Real damage: Lower limits spike utilization, crush scores, and raise costs on mortgages, auto loans, and other card lines.

For South Florida professionals who run their lives through MIA and FLL on a weekly basis, these instant line cuts aren’t just an inconvenience, they’re a systemic risk to business continuity. In a world already packed with deadlines, travel delays, and client obligations, no one has the time or energy to constantly worry about their own credit card company turning against them. American Express’s automated system makes every billing cycle a gamble: a small blip on your credit report, or a payment delayed by a day, can set off cascading disruptions. Instead of peace of mind, cardholders live with the anxiety that their financial lifeline could be pulled at any moment, forcing them to scramble for cash, juggle accounts, and divert focus away from the work and travel that actually matter. It’s a headache no serious professional needs in an economy that already demands resilience.

What makes this worse is the hypocrisy baked into American Express’s own brand. The company still floods the market with ads promising to be the card for business leaders, global travelers, and professionals who “never stop moving.” Yet behind the glossy marketing, the reality is the opposite: a rigid computer system that punishes the very people Amex claims to serve. The entrepreneurs running payroll, the consultants flying out of MIA and FLL, the small business owners who put six figures a year on their Amex for points and perks, these are the same people blindsided by line cuts that wreck cash flow and trip up travel. The disconnect is glaring. Amex sells stability but delivers volatility. It markets loyalty but rewards suspicion. It positions itself as a premium tool for professionals, but in practice it has become a constant liability, a company whose algorithms attack its most loyal customers without warning, and without reason.

What This Means for Consumers

When credit lines move like quicksand, your entire financial plan can collapse in a split second.

Cash-flow whiplash: A $10,000 reduction can break a payroll, cancel a supplier payment, or derail a trip.

Credit-score hit: Utilization jumps when limits fall, harming your FICO and raising borrowing costs.

Operational risk: Entrepreneurs and frequent travelers, the very customers Amex courts, get ambushed mid-itinerary.

Bottom Line: You Can Not Trust American Express

At the end of the day, American Express has become a liability no professional or consumer should carry. As a charge card, it is supposed to provide reliability and strength. Instead, it has devolved into a system where tens of thousands of dollars in credit can vanish without warning, leaving you stranded with no explanation, no recourse, and no support.

During these crises, Amex does not step in to help. Instead, they demand access to your bank accounts through automated pulls, while customer service agents admit they are powerless to override the algorithm. Even after large payments, $10,000 or more, cardholders report those funds effectively “disappearing,” offset instantly by a matching credit line reduction. The money goes into Amex’s accounts while you are left high and dry, unable to access your own financial cushion.

American Express once sold itself as “the card you never leave home without.” Today, it’s the card most likely to leave you stranded, because an opaque risk engine decided to pull the rug out without warning. If you value stability and respect from your financial partners, reconsider Amex. The company that promised white-glove service has turned into a black-box surveillance machine that punishes loyalty at scale.

If you can afford to lose $10,000 in the blink of an eye, maybe this is the card for you. But for anyone who values stability, trust, and customer support, American Express is not the card for 2025. This is a company that charges some of the highest annual fees in the industry not to protect you, but to subject you to algorithmic punishment and bureaucratic stonewalling.

The truth is simple: in 2025, you would have to be a fool to carry an American Express card.

Here are some of the sources documenting American Express’s widespread practice of cutting credit lines without warning:

- Reddit: “Drastically reduced credit limit with NO notice”

- Reddit: “Amex lowered limits on all cards?”

- Reddit: “Amex slashed credit limit across all cards”

- Reddit: “AmEx randomly decreased my credit limit”

- Reddit: “American Express lowered my credit card limit after a large purchase”

- BBB Complaints: American Express — credit limit reduction complaints

- BBB Complaints: Additional examples

- BBB Complaints: Disputed rationale for limit cut

- CFPB Complaint (global limit cuts)

- CFPB Complaint Database (Amex; multiple narratives)

- WalletHub explainer: “Amex lowered my credit limit”